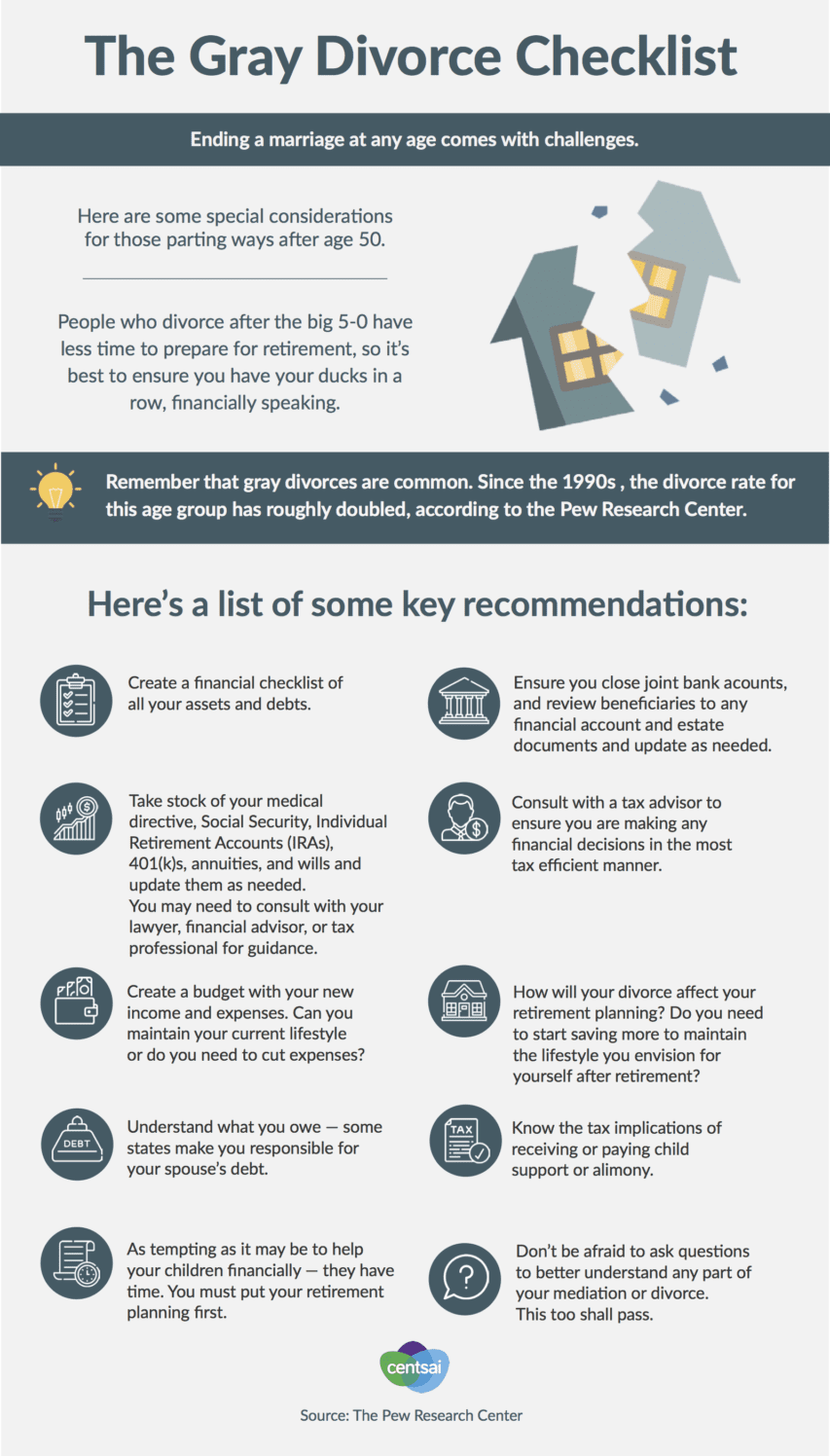

Gray Divorce: Charting a Course Towards a Secure Financial Future

As society evolves, the phenomenon of “gray divorce” among Gen Xers and Baby Boomers is becoming increasingly common. Beyond the emotional toll, the aftermath of a long-term separation poses significant financial challenges that require careful steering through a maze of tricky parts, tangled issues, and confusing bits. This opinion editorial explores how individuals facing a gray divorce can manage their money with composure and foresight, offering practical advice on budgeting, downsizing, rethinking Social Security, pursuing work opportunities, and preparing for long-term care—all while avoiding money mistakes that could derail a secure retirement.

Here, we aim to provide readers with actionable insights by diving into the nitty-gritty details of financial planning during this transformative phase of life. We take a closer look at the key decisions that need to be made and examine the subtle distinctions that can significantly impact one’s financial stability in later years.

Redefining Your Budget in the Wake of Divorce

One of the first steps after a gray divorce is to take a closer look at your finances and create a new budget that reflects your changing circumstances. The cash flow enjoyed during your marriage likely supported one household, but post-divorce you will now need to make your way through managing two separate living expenses. Although you are primarily responsible for your own costs, some expenses—such as housing, insurance, and healthcare—may now take up a higher percentage of your income.

Rather than being overwhelmed by the twist and turns of recalibrating your budget, consider breaking down the process into manageable stages:

Step-by-Step Budget Reassessment

- Itemize Fixed Costs: Start by listing long-term expenses like rent or mortgage payments, car loans, insurance premiums, groceries, and utilities.

- Reevaluate Variable Expenses: Identify costs that can be adjusted—dining out, travel, entertainment, and gifts—and determine how these might be scaled back or modified in your new financial scenario.

- Prepare for Unexpected Expenses: Set aside funds for emergencies, particularly as you may now face unexpected costs on your own.

By diving into these little details with a clear table or spreadsheet, you can create a comprehensive overview of your finances. This practice not only simplifies the process but also reduces the nerve-racking uncertainty that typically accompanies significant life changes.

Considering Downsizing: Weighing the Pros and Cons of Selling the Family Home

Many individuals in a gray divorce may hold on to the idea of maintaining the family home, often laden with memories from the past. However, keeping such a large property can be intimidating for your wallet. Not only might retaining the home mean a significant reduction in the distribution of equity, but the costs associated with upkeep, taxes, and a potential mortgage can also squeeze your budget.

With a realistic view of your future finances, it may be more beneficial to consider selling the property and opting for a downsized residence. This transition could serve as a springboard toward a more manageable lifestyle. When evaluating your housing options, consider these points:

Downsizing: Benefits Versus Hidden Complexities

| Benefits | Challenges |

|---|---|

|

|

Taking the wheel and making informed decisions in this area can help you avoid being house-poor. By carefully considering the financial pros and cons, you can steer through the complicated pieces of homeownership in a way that aligns better with your post-divorce goals.

Understanding Social Security Divorce Benefits in Later Life

For couples who have been married for at least 10 years, Social Security benefits can offer a critical financial lifeline after divorce. Specifically, eligible individuals are entitled to receive either their own Social Security benefit or up to half of their former spouse’s benefit, whichever amount is greater. This provision can be a major factor in long-term financial planning, particularly for those who approach retirement age.

It’s important to appreciate the fine points of this arrangement by considering your timing and personal circumstances. For instance, if you have been married for just under the qualifying period, you might consider delaying the final divorce decree to maximize this benefit. Equally, the decision regarding when to initiate Social Security benefits—whether to claim early and receive a lower monthly payout or wait to enjoy a higher benefit—depends largely on your financial needs and anticipated longevity.

Here are a few aspects to consider when evaluating Social Security decisions post-divorce:

- Marital Duration: A few extra months might make a significant difference if you’re on the boundary of the 10-year requirement.

- Timing of Benefits: Consider whether drawing your benefits as soon as possible meets your needs or if delaying could yield a more robust monthly payment.

- Personal Financial Situation: Assess your overall assets, living expenses, and expected health trajectory before making decisions.

In managing your way through these decisions, it’s super important to conduct a detailed evaluation of both immediate and future needs. Working with a financial planner can help clarify these subtle details and ensure that your choices are in line with your long-term security.

Finding New Opportunities: Working After Divorce

It’s not uncommon for a gray divorce to radically alter your income stream, making it necessary to explore alternative sources of revenue. Whether the decision to return to work full-time is driven by necessity or a desire for renewed purpose, re-entering the workforce or supplementing your income through part-time opportunities can be an effective strategy.

The concept of working after divorce is not merely about adding extra dollars to your bank account—it is about regaining control and paving a path that allows for increased flexibility in retirement planning. For many, the idea of prolonged career engagement may feel off-putting at first; however, there are several less demanding options available:

Exploring Alternative Work Options

- Part-Time Engagements: Consider roles such as substitute teaching, consulting, or even freelance work that matches your skill set without the pressures of full-time employment.

- Flexible Schedules: Look for opportunities that offer flexibility, allowing you to balance work with personal time – a critical component of your post-divorce lifestyle.

- Remote Work: With advancements in technology, many jobs now offer remote options that minimize commuting costs and stress.

Supplementing your income through part-time work not only helps maintain your current lifestyle but might also allow you to delay drawing on investments and savings prematurely. Essentially, keeping a steady income can provide a buffer during the transition, affording you the chance to cope with the little twists and turns that accompany this phase.

Securing Long-Term Care: Planning for Future Needs

When facing life as a single individual, long-term care insurance becomes a key component of your financial security strategy. Unlike the shared responsibilities of a marital partnership, managing long-term care expenses on your own requires planning and, often, making potentially intimidating decisions at a relatively young age.

The prime objective is to secure coverage before health issues or age-related challenges escalate the costs. For individuals under the age of 60 who are still in good health, it makes sense to invest early in long-term care insurance. For those worried about premiums, negotiating the waiting period (such as opting for a period of 180 or 360 days) can be a manageable compromise.

Here are several strategies to consider when planning for long-term care:

- Early Enrollment: Purchasing coverage while you are younger and healthier can result in lower premiums and a smoother approval process.

- Extended Waiting Periods: If premiums are beyond your budget, a longer waiting period may allow you to postpone benefits, reducing the immediate cost.

- Policy Conversion Options: Some policies offer an option to exchange a life insurance policy for a long-term care policy, which can be a viable alternative if traditional policies prove to be too expensive.

Additionally, some individuals may consider transitioning into a “continuing care” retirement community that provides various levels of support as time passes. This approach allows you to start with independent living and gradually move to more assisted care settings as needed. While there are many fine shades to consider within the long-term care spectrum, planning in advance can alleviate the nerve-racking pressure of unanticipated health needs.

Charting a Path Through the Hidden Complexities of Divorce Financial Planning

The overall process of untangling one’s financial future post-divorce is filled with complicated pieces and subtle parts that can significantly impact retirement outcomes. The journey is often loaded with issues, including the need for professional legal advice, disputes over asset division, and the careful balancing of budgets that once worked seamlessly for two. An early decision that is both off-putting and overwhelming might be to forego hiring experienced professionals in a bid to avoid legal fees. However, lacking professional guidance could indeed cost much more in the long run.

Engaging an experienced divorce attorney is not merely a luxury; it is a must-have step in ensuring that your rights are protected and your financial interests are prioritized. The professional advice you receive can help you figure a path through important decisions—from the equitable division of assets to the understanding of tax consequences that come with a gray divorce. In many cases, the upfront costs may pale in comparison to the potential pitfalls avoided later on.

Key Steps to Stay on Track: A Practical Checklist

To help you work through these tricky parts, take a closer look at the following checklist that summarizes the essential steps in managing your finances after a gray divorce:

- Budget Adjustment: Evaluate and realign your income streams, focusing on both fixed and variable costs to better reflect your new financial reality.

- Housing Decision: Decide whether to keep or sell your family home by weighing the emotional costs against the financial benefits of downsizing.

- Social Security Planning: Understand the fine points of Social Security divorce benefits and decide the optimal time to claim these benefits.

- Employment Opportunities: Consider returning to work or supplementing your income with flexible, part-time roles to delay dipping into your retirement funds.

- Long-Term Care Protection: Secure long-term care insurance early or explore alternative options such as policy conversion or retirement communities.

- Professional Guidance: Retain a seasoned divorce attorney and financial planner to help you make informed decisions during this critical time.

Each of these bullet points represents more than just an action item—they serve as building blocks for a new financial strategy that accommodates your evolving needs. Whether you’re negotiating tangled issues relating to asset distribution or reconsidering your work-life balance, every step you take now is critical.

Strategic Financial Advice: Engaging with Professionals

Engaging financial advisors, legal professionals, and retirement planners early in your post-divorce process can be incredibly beneficial. These experts can help you poke around and understand the subtle parts of your evolving financial landscape, ensuring that all aspects are thoroughly considered. Whether it’s deciphering the small distinctions between various investment strategies or making sense of the nitty-gritty details of tax implications, professional guidance turns overwhelming tasks into manageable steps.

Professionals in this arena bring a wealth of experience to the table. Their insights can be particularly useful when it comes to negotiating or reevaluating certain divorce outcomes, such as asset division or long-term care insurance options. The investment in quality advice today could very well avert considerable financial challenges down the line.

Managing Emotional and Financial Risks in Gray Divorce

It is important to acknowledge that financial planning after a divorce is not just about the math—it is equally about managing the emotional impact of significant life changes. An overwhelming sense of loss or stress can make it difficult to figure a path forward. The dual pressures of handling emotional upheaval and managing practical expenses often create a situation that feels full of problems.

In these tense times, taking methodical steps can help balance your psychological well-being with the practical needs of your financial situation. Steps include:

- Seeking Counseling: Consider professional therapy or financial counseling to work through both emotional and fiscal strains simultaneously.

- Regular Review: Schedule periodic reviews of your budget and long-term plans, giving you a clear sense of control and direction even when circumstances shift.

- Building a Support Network: Cultivate relationships with peers, support groups, or financial mentors who have navigated similar life changes with success.

By adopting a holistic approach that marries emotional resilience with careful planning, you can reduce the likelihood that money mistakes—whether big or small—will derail your efforts to prepare adequately for retirement.

Adapting to a New Financial Landscape: The Role of Flexibility

Flexibility is a critical asset during any major life transition, especially following a gray divorce. Your financial landscape may now require adjustments on the fly, as rigid plans can quickly become obsolete when confronted with new challenges or unexpected expenses.

Here are some ways to ensure that your financial strategies remain flexible and resilient over time:

- Dynamic Budgeting: Regularly update your budget to reflect new challenges and opportunities. A budget that adapts to your current income and expenses can be a powerful tool to manage uncertainty.

- Reassessing Investments: Periodically review your retirement savings and investment allocation to ensure they align with your evolving risk tolerance post-divorce.

- Staying Informed: Keep up with changes in tax laws and Social Security regulations. Being well-informed helps you make better decisions as policies change over time.

- Contingency Planning: Build an emergency fund that can cover unexpected medical expenses or other surprises without jeopardizing your long-term financial plan.

Making your finances flexible means being willing to alter strategies when the situation demands it. With a flexible mindset, you can figure a path through sudden changes and ensure that even nerve-racking uncertainties are met with strategic planning.

Practical Wisdom: Balancing Practical Needs with Professional Advice

After a gray divorce, it’s important to embrace the wisdom gained from years of experience while also seeking fresh perspectives from professionals who are current on the latest trends. This balance of practical wisdom and professional insight is essential for managing the small distinctions and unexpected twists that arise in financial planning.

Consider these practical pieces of advice:

- Do Not Rush Decisions: Take the time you need to understand every financial twist and turn before making a decision. Quick fixes may lead to regret later on.

- Review and Revise: Financial planning is not a one-time event but an ongoing process. Periodically review your plans and adjust them based on your changing circumstances.

- Be Patient: Realize that building a secure financial future takes time, and the gradual process of managing bills, meeting savings targets, and planning for long-term care should be approached with patience and consistency.

- Educate Yourself: The more you understand about the subtle parts of financial planning, the better equipped you will be to make decisions that benefit your long-term well-being.

Taking the time to both digest and apply this advice can transform what initially seems like a nerve-racking situation into a well-organized plan tailored specifically for your needs.

Future-Proofing Your Finances After Divorce

Looking ahead, the goal for anyone undergoing a gray divorce should be to build and maintain a resilient financial foundation. This means not only addressing the immediate challenges of budgeting and asset division, but also considering disruptive factors such as healthcare costs, evolving Social Security policies, and unpredictable economic conditions.

Future-proofing your finances involves developing strategies that can withstand evolving circumstances. Consider these tactics:

- Regular Financial Reviews: Schedule annual or semi-annual reviews with your financial advisor to revise your plan according to your current needs and market conditions.

- Diversification: Spread your investments across a variety of assets to mitigate potential risks and ensure that your retirement savings are robust, even in a changing economy.

- Adaptive Planning: Create scenarios for various future events—such as changes in tax laws or unforeseen health issues—and develop contingency plans accordingly.

- Staying Organized: Keep all financial documents organized and easily accessible. This makes it simpler to adapt quickly if changes occur.

The combination of these strategies can help soften the blow of unexpected challenges and secure your financial future well into retirement. Future-proofing your finances is about continuously reassessing and adapting your strategies so that you are never left unprepared.

The Bottom Line: A Roadmap for Success After Gray Divorce

In conclusion, while gray divorce brings with it a host of challenging parts and complicated pieces, the need for a carefully crafted financial strategy is clear. Whether it’s reworking your budget, making decisions about your family home, understanding the full small distinctions of Social Security benefits, exploring alternative work arrangements, or planning for long-term care, every decision matters.

Here is a concise roadmap to guide you:

- Engage Professional Help: Retain an experienced divorce attorney and financial planner early to help you make informed decisions.

- Redefine Your Budget: Itemize fixed and variable expenses, and adjust for the reality of living on your own.

- Reassess Housing Needs: Evaluate whether keeping the family home is financially beneficial or if downsizing could provide a more suitable living situation.

- Plan Social Security Benefits: Understand the rules and timing to maximize your post-divorce benefits.

- Explore Incomes Opportunities: Determine whether returning to work or supplementing your income part-time suits your lifestyle.

- Invest in Long-Term Care: Secure insurance or alternative arrangements before health challenges escalate.

By following these steps, you can make your way through the tangled issues of a gray divorce while keeping your financial future as a strong priority. Success in this new phase is not simply measured by how quickly you bounce back, but by how effectively you secure a stable, balanced life for your retirement years.

Ultimately, every gray divorce is a chance to start afresh—reinventing not just your living situation but also your approach to financial security and personal well-being. While the path forward is certainly loaded with twists and turns, taking a measured, informed approach will help ensure that your hard-earned resources are preserved for the years to come.

Looking Ahead: The Promise of a New Beginning

In the end, a gray divorce is not only a dissolution of marital ties but also an opportunity for reinvention and renewed focus on what truly matters. With the right balance of practical advice, professional guidance, and personal resolve, you can manage your finances wisely and construct a retirement plan that reflects the complexities and wonders of your life’s next chapter.

By getting into the fine points of your financial world and tackling each of these significant decisions head-on, you set yourself on a path to secure, sustainable wealth—a goal which remains super important as you redefine your future. With clear, deliberate steps, what once appeared overwhelming can be transformed into a manageable, stable opportunity for growth and security.

In this new era of independence, every strategic decision you make is a building block toward a financially sound and fulfilling retirement. While the journey may sometimes seem intimidating and off-putting, remember that every small step—when combined with professional advice and persistent effort—brings you closer to achieving the secure, comfortable future that you deserve.

As our society continues to evolve and more individuals face the complicated pieces of gray divorce, the overall lesson remains clear: careful planning, flexibility, and proactive measures are your best tools for ensuring that your post-divorce financial life is not defined by loss but by resilience and growth.

Ultimately, the financial journey post-divorce is one that requires balance—balancing emotional healing with practical steps, past experiences with future goals, and established habits with innovative solutions. With each choice you make, you not only reclaim your independence but also pave the way for a retirement that honors both your past and your potential for tomorrow.

Originally Post From https://fortune.com/2025/04/08/gray-divorce-gen-x-boomers-5-money-mistakes-to-avoid/

Read more about this topic at

Decoupling Your Finances: How to Divide Your Money in a …

Navigating the Financial Waters of Divorce